Job volumes are declining as the labour market is cooling

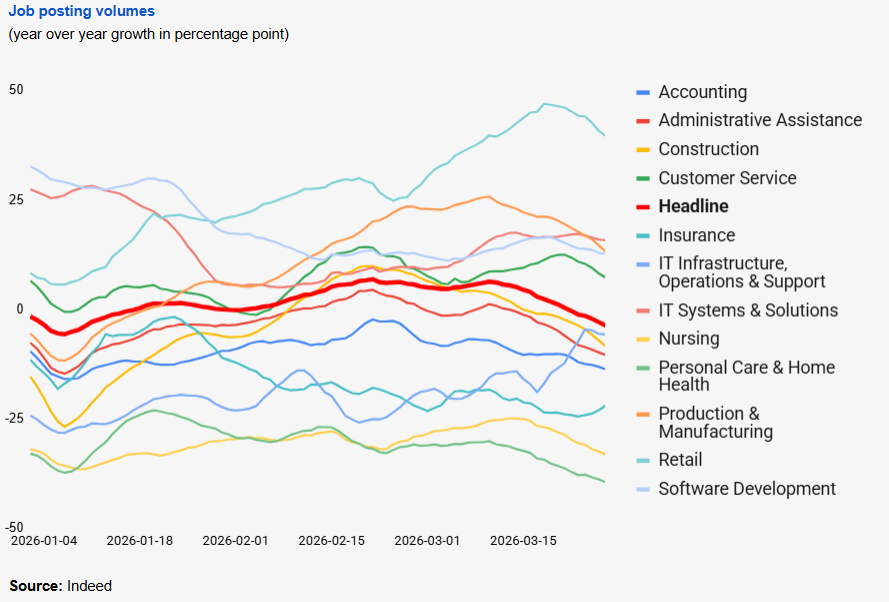

The Canadian labour market is exhibiting clear signs of cooling, as evidenced by a steady contraction in job posting volumes over the early months of 2026. Data compiled from Indeed job postings tracks year-over-year percentage changes across diverse employment sectors, offering a real-time window into hiring demand. The headline index, represented by the prominent red baseline, indicates that overall hiring activity has shifted into negative territory after a brief stagnation. Over the last four weeks leading into late March 2026, the aggregate trend line dipped below the zero mark, confirming that total job openings are actively shrinking compared to the same period in the previous year. This deceleration aligns with broader macroeconomic headwinds, including sustained restrictive monetary policy by the Bank of Canada and a general softening in domestic consumer spending.

A granular analysis of individual sectors reveals a stark divergence between highly cyclical industries and defensive, specialized fields. The standout performer through the first quarter of the year is the insurance sector. Job postings for roles such as claims managers and underwriters surged dramatically, peaking near a forty-five percent year-over-year increase before experiencing a slight moderation in the final weeks of the period. This resilience highlights the non-discretionary nature of insurance services, which often experience consistent demand or even heightened operational activity during periods of economic restructuring and risk management.

Conversely, consumer-facing and tech-related sectors are bearing the brunt of the economic slowdown. Retail job postings have remained deeply depressed, hovering between twenty and thirty percent below prior-year levels throughout the entire timeline. This persistent deficit reflects a cautious approach by retailers as Canadian households scale back discretionary expenditures in response to high debt-servicing costs. Similarly, software development postings started the year with modest positive growth but experienced a sharp, continuous decline, ultimately plunging well into negative territory by late March. This trajectory mirrors the broader global recalibration within the technology sector, where firms have transitioned from rapid headcount expansion to cost optimization and automation.

Subscribe now for free and have access to all our stories, enjoy exclusive content and stay up to date with constant updates.